When global investors picture China’s capital markets, names like Alibaba, Tencent, BYD, and AI leaders such as DeepSeek immediately come to mind. Yet the companies that truly drive China’s core domestic equity benchmarks are far different: older, heavier, and deeply state-linked. These state-owned banks, energy giants, and insurers form the backbone of the world’s second-largest economy. And remain largely overlooked by most foreign investors. Understanding this divide begins with how China’s major indexes are constructed, much like the U.S. Dow Jones or S&P 500.

This article investigates why China’s domestic stock-market benchmarks remain dominated by state-owned banks, energy companies, and insurers rather than the technology platforms that dominate global headlines. It explains the structural economic reasons why “Old China” continues to anchor mainland equity indices despite the rise of Alibaba, Tencent, and AI stocks.

China Has No Dow Jones. The CSI 300 and FTSE China A50 Come Closest

The Dow Jones Industrial Average (DJIA) is a price-weighted index of 30 large U.S. companies. China has no direct equivalent. No single government-endorsed benchmark of a fixed number of national champions functions as the universal standard.

The closest practical comparisons are the CSI 300 Index (or Hushen 300 Index) and the FTSE China A50 Index, both of which track A-shares, renminbi-denominated stocks listed on the Shanghai (SSE) or Shenzhen stock exchanges (SZSE), available primarily to mainland Chinese investors and qualifying international funds.

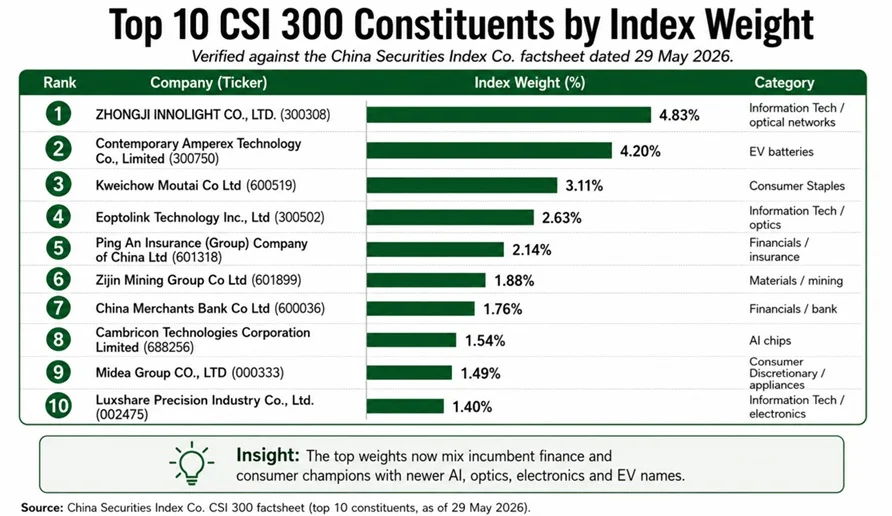

The CSI 300, compiled by China Securities Index Co., tracks the 300 largest and most liquid A-shares by market capitalization and covers approximately 70% of the mainland market. Launched in 2005, it stands as China’s nearest practical equivalent to the S&P 500. The top ten largest CSI 300 companies by weight are listed out in the infographic below.

The FTSE China A50, launched in 2003 by FTSE Russell. It tracks the 50 largest A-share companies and, according to FTSE Russell, accounts for “over one-third of its total market capitalization […] making it a key barometer of China’s economic and equity market performance.” FTSE Russell has also confirmed that “nearly 60% of Assets under Management (AuM) in globally issued China Exchange Traded Funds (ETFs) track a FTSE China index.”

Unlike the price-weighted Dow, both Chinese indexes are market-capitalisation-weighted, meaning the largest companies by market value exert the most influence over daily movements.

The State Still Moves the Market: Why Old China Controls the Indexes

China’s A-share market reflects the country’s economic structure: one in which the state retains controlling stakes in the country’s most systemically important institutions through the State-owned Assets Supervision and Administration Commission (SASAC).

Banking in China, for example: China’s Big Four state banks, Industrial and Commercial Bank of China (ICBC), China Construction Bank (CCB), Agricultural Bank of China (AgBank), and Bank of China (BoC), function as instruments of industrial policy as much as commercial lenders. They channel credit toward infrastructure, agriculture, housing, industry, and strategic industries at rates guided by central government priorities.

The financial sector represents approximately 23–30% of CSI 300 by weight, its single largest allocation. Though the sector has historically been even more concentrated in the 50-stock FTSE China A50. Energy and utilities add a further meaningful share, leaving both benchmarks heavily skewed toward the tangible economy (credit, fuel, coal, and power) rather than consumer apps or cloud platforms.

As S&P Global data confirms, “The four largest banks in the world are all Chinese state-owned lenders: ICBC, Agricultural Bank of China, China Construction Bank, and Bank of China. Together, those four institutions hold $25.5 trillion, or roughly one-quarter of the $101.6 trillion total of the top 50 banks,” a market report noted.

The Old China Titans: ICBC, PetroChina, Ping An and the Giants Moving A-Shares

Industrial and Commercial Bank of China (ICBC), founded in 1984 and majority state-owned, is the world’s largest bank by assets. In 2026, ICBC reported total assets surpassing 53 trillion yuan (~$7.7 trillion), making it the first bank globally to cross that threshold. It plans to distribute approximately 110.6 billion yuan in dividends for 2025. At the bank’s results briefing, ICBC’s Liu Jun, vice-chairman and president, stated: “If the market calls for a higher payout ratio, ICBC, as a bellwether, will take the lead in responding.”

China Construction Bank, Agricultural Bank of China, and Bank of China complete the “Big Four” state lenders. Together with ICBC and two smaller peers, China’s six largest state banks are set to distribute a combined record over 427 billion yuan (~$61 billion) in dividends for 2025.

PetroChina, controlled by China National Petroleum Corporation with an 82.6% stake, carries a market capitalization of approximately $242 billion at the time of writing and generated over $400 billion in revenue in 2024. Sinopec, with the largest petrol station network of over 30,000 locations, operates as the world’s largest oil-refining conglomerate by scale and is administered by SASAC. China Shenhua Energy, the largest coal producer and dominantthermal power company, carries a market capitalization of approximately $139 billion at the time of writing.

Ping An Insurance, a constituent of both the CSI 300 and FTSE China A50, ranked 29th on the Forbes Global 2000 in 2024 (rose to 27th in 2025). and provides life, health, property, and banking services across China.

China Merchants Bank (CMB) has positioned itself as the country’s leading retail bank by wealth management penetration, with retail assets under management rising 12% year-on-year in 2024. In March 2026, its board committed to distributing 35% of first-half 2026 net profit to ordinary shareholders.

Why Alibaba and Tencent Do Not Speak for China’s Mainland Stock Market

A common misconception is that China’s stock-market performance mirrors the fortunes of its global technology names. Alibaba and Tencent are not listed on mainland A-share exchanges. As Allianz Global Investors has noted, “many internet giants – such as Alibaba and Tencent – are only listed in offshore markets.” Both trade in Hong Kong and via American Depositary Receipts (ADRs) in New York, placing them entirely outside the CSI 300 and FTSE China A50, as part of the “New China,” which we will discuss in our next piece.

J.P. Morgan Asset Management has observed that onshore equities carry a structural income advantage, with energy and financial sectors offering “up to 6.7% and 4.8% dividend yields, respectively.” With China’s 10-year government bond yield falling toward ~1.7-1.74%, that spread has drawn domestic institutional and retail flows into state-owned companies that international investors frequently overlook.

What Old China Means for Investors: 7% Dividend Yields, Property Exposure and Policy Backstops

Dividend yields. With the People’s Bank of China maintaining a low-rate environment, the gap between bank deposit rates (below 2%) and state enterprise dividend yields (5–7%+) continues to attract mainland institutional buyers, particularly life insurers and pension funds.

Property-sector exposure. State bank loan books retain significant real estate lending exposure. Non-performing loan ratios across the Big Six banks remained below 1.34% through Q3 2025, but trajectory and property sector recovery pace remain central risk factors.

Next, energy and infrastructure spending. Central government capital allocation toward energy security and grid capacity provides long-term revenue visibility for PetroChina, Sinopec, and China Shenhua, all of which carry implicit state support backstops.

Lastly, Regulatory evolution. Since China began easing pressure on technology companies after 2023, FTSE Russell and CSI index rebalances have started to give more room to AI and semiconductor stocks. But benchmark composition changes slowly. The shift is happening over several quarters, not in a matter of months.

The Bottom Line: Old China Still Is the Market

China’s equity narrative runs on two tracks. The offshore Hong Kong market tells the story of Alibaba, Tencent, and DeepSeek. The mainland A-share benchmarks, the CSI 300 and FTSE China A50, tell the story of the state-owned giants that have financed, fuelled, and insured the world’s second-largest economy for decades.

For investors seeking real exposure to China’s domestic equity market, these companies, not the technology platforms dominating Western headlines, deserve attention. And understanding Old China isn’t optional anymore. It is the market.

Author: Richardson Chinonyerem

The editorial team at #DisruptionBanking has taken all precautions to ensure that no persons or organisations have been adversely affected or offered any sort of financial advice in this article. This article is most definitely not financial advice.

See Also:

Are Dow Jones Components Targets for Activist Hedge Funds? | Disruption Banking